Brazil imports 50 percent of the phosphates it needs for agricultural production: MBAC has the ability to become the second largest domestic producer of single superphosphates within the next five years, with a valuable sideline in rare earth elements.

In the field of mining and resources it takes a bold and entrepreneurial mind to enter a large and established market as a new entrant. You really have to understand the business and the territory you are operating in. When MBAC was founded in 2008 to enter the Brazilian fertilizer market it was built by a team with impeccable credentials.

Antenor Silva, CEO and vice chairman, has over 40 years’ experience in the mining and chemical industries of Brazil and is instrumental in the development of four out of five of its operating phosphate mines and the country’s only potash project. Roberto Busato Belger adds another 32 years in the industry, having been chief operating officer of Fosfertil Fertilizantes, Latin America´s largest supplier of phosphate and nitrogen for fertilizer production, and before that pursuing a very successful career with the global agribusiness corporate Bunge. He is now president and COO of MBAC.

Both Silva and Belger are Brazilians: this is a team with a unique understanding of the market for phosphates and how to set up and run a project in Latin America. The decision to base the company in Canada will be well understood by anyone who works in mining. “People who invest on the Toronto Stock Exchange truly understand risk investing – they typically are more comfortable in investing in early stage projects,” says Steve Burleton, VP of Corporate Development. Canada is an agricultural economy which understands fertilizers, but to acquire its first project MBAC went first to private investors, and following an initial funding round purchased a small scale mining and processing operation called Itafós Mineração Ltda, near the border of Goiás and Tocantins States in central Brazil.

The company floated on the TSX the following year, 1999, and since then has been operating the current Itafós mine, though its growth is largely projected on an associated project. The Itafós mine has been producing about 50,000 tonnes per annum of rock phosphate, which requires little processing, and is crushed and sold to local farmers for direct application to their land.

It is worth looking here at the way demand for phosphates is likely to develop in Brazil. The country is becoming the bread basket of the world, and consequently one of the great opportunities in the agricultural sector today, says Burleton. “Brazil is one of the few places in the world where you can dramatically grow cropping space while other countries are losing it to urbanisation.” Accordingly the demand for crop nutrients is certain to grow above normal rates.

Perceiving this, the giant Brazilian mining conglomerate Vale doRio Docemoved into the market in 2010, acquiring the phosphate operations of both Bunge and Fosfertil in preparation for meeting the lion’s share of this burgeoning market. MBAC will be one of the significant competitors, and has growth plans that Burleton is confident will make it the second largest player in Brazil. After the end of 2012 its product will no longer be rock phosphate but the more concentrated single superphosphate (SSP) which will be produced at a new facility on the same property. Once this is up and running the existing plant will be closed, he says.

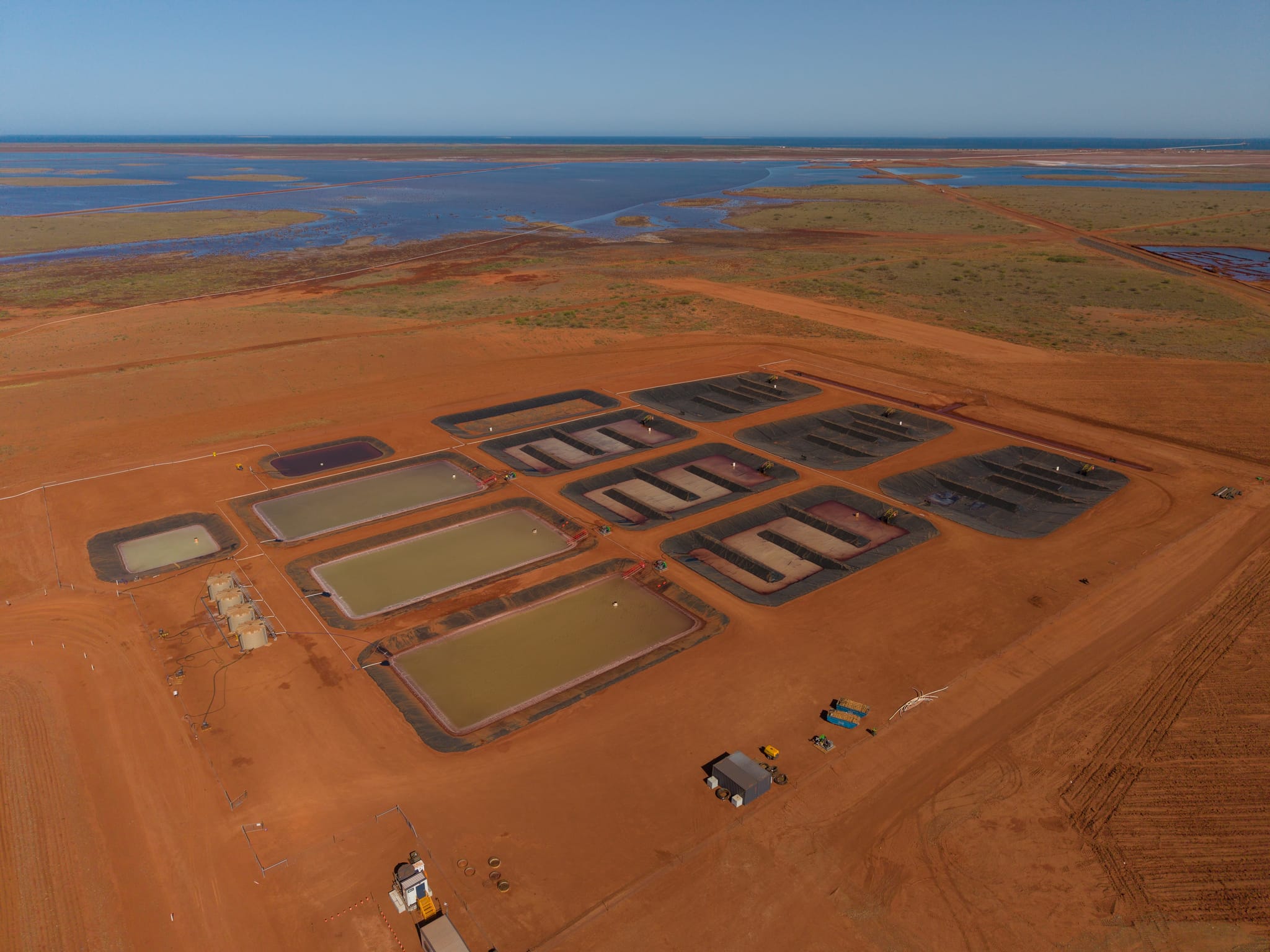

The Itafós Arraias SSP Project (so called because it is near the town of Arraias, around eight miles from the existing plant) includes a new mine and mill facility, a sulphuric acid plant, an SSP plant and a granulation plant. At full capacity, the mine will produce 500,000 tonnes of SSP a year. Once that has been achieved, MBAC then will consider a second phase of development raising output at Itafós to one million tonnes as early as 2015.

Itafós is a fast track project, helped by the groundwork that has gone into getting it fully funded and permitted and the fact that it is using mainly off-the-shelf technology. The sulphuric acid plant that beneficiates the rock into SSP, for example, is identical to one installed last year in the United States. Once it is running later this year it will employ about 500 people, and its environmental impact will be low – though it is an open pit it works like a strip mine, Burleton explains, where the land is rehabilitated progressively. “One of our lenders is the IFC, which is part of the World Bank. They have the highest environmental standards and work to the Equator Principles of environmental risk management. We have to report quarterly that we are following those but we are very confident we can meet their very high standards.”

But this is far from the only project MBAC has. Its second development is the Santana Project, located in the south-east of Pará State. From here it is well placed to supply demand from the northern and eastern regions of Mato Grosso State, the major soya bean production region in Brazil and Pará State, which is the focus for beef production.

Dicalcium phosphate (DCP) produced at the plant is a high margin product much in demand from cattle farmers in Brazil. “In our Santana project we will have the ability to make phosphoric acid which means that we will be able to make DCP and take advantage of that demand.” Initial results indicate that Santana could yield at least as much SSP as Itafós, and MBAC is already in talks with one of Brazil’s largest animal feed companies to supply DCP. Santana has a strong logistical advantage: currently most of the fertilizer brought into the region is imported through Paranaguá Port 2,150 kilometres away. The only other potential sources are in southern Minas Gerais State which is approximately 1,000 kilometres distant or through Itaquí Port 1,400 kilometres away in northern Brazil.

A third project in the south, in Minas Gerais State close to Vale’s major phosphate operation at Araxá is also expected to yield high grade phosphate ore. However the 70-100 metre layer that sits above the phosphate rock and that would have to be removed to access it has been shown to contain a world class resource of niobium, increasingly in demand for steel production and electronics applications, and rare earth oxides (REOs).

MBAC remains focused on phosphates so this added value was a happy coincidence – the discovery came out of the original due diligence process. “The phosphate resource was very interesting – perhaps 100 million tonnes at ten percent grade which in Brazil is an excellent deposit – but when we looked at some of the drill results above that we found a very high quality rare earth/niobium deposit sitting on top in what would otherwise have been waste rock.” Araxá sits between Vale’s phosphate mine and the operations of Companhia Brasileira de Metalurgia e Mineração (CBMM) which supply 85 percent of global niobium requirements. So apart altogether from the value of the resource itself, it has the advantage of excellent infrastructure and an experienced workforce in the area.

Many of the world’s rare earth projects are very remote, contain only a few of the elements in the group, and are of much lower grade than Araxá. Historical drilling at the project recorded only yttrium, lanthanum and cerium, though these were present at 6.6 percent concentration, in contrast with the two or three percent grades that characterise many other deposits, according to Burleton. What is more exciting though is the total rare earth oxide or TREO rating, which is indicated to reach between eight and nine percent. This is close to being confirmed: MBAC has already carried out 2,000 metres of drilling and is in the process of drilling another 1,000 metres. “Our goal is to have a preliminary economic assessment on the full suite of REOs out later this year,” he says.

Confirmation at anything like these grades will undoubtedly add value to the company’s stock. MBAC’s goal over the first half of 2012 following further sampling to determine the incidence of all 15 rare earth oxides will be to go to the market with a view to entering off-take agreements for these elements. In the present climate that is not hard to do: the world automotive industry and the Chinese manufacturing supply chain will bite the hand of any supplier that can offer a reliable and accessible supply of rare earths. More importantly, Burleton points out, off-take agreements will help establish the credibility of the project.

This is a company in great shape. Its first new development at Itafós Arraias is fully funded and on track to be generating significant cash flow by the end of this year, and this alone differentiates it from other players in the fertilizer space. It has a near term project that is going to be generating significant cash flow and two other exciting growth projects. “We are very interested in listing in Brazil but we need to get a bit bigger first,” says Burleton.” In August 2011 MBAC listed on the OTCQX International in the United States, the premium tier of the US over-the-counter (OTC) marketplace. “This was to expand our investor base,” he explains. Currently 85 percent of the stock is held by institutions or by the management and directors of the company but he feels the time is right to expose the company to the retail market as well.

DOWNLOAD

MBAC-AM-Bro-s.pdf

MBAC-AM-Bro-s.pdf